£6,000 today… or £10,000 for your future?

Following my recent post about pension tax relief, I received several messages asking how it works.

So, I thought I would put this together and explain it properly so you can see whether this applies to you and whether it is worth exploring further.

A quick clarification

I am not a pension advisor, and I am not advising on which pension products to choose.

This article focuses on how the tax system works when you contribute to a pension and how the available reliefs apply. What you choose to do with your money is always a personal decision.

What’s happening once you earn over £50k

As it stands, the basic rate band is £50,270 (at the time of writing).

In simple terms:

• The first £12,570 is tax-free

• Above this and up to £50,270 is taxed at 20%

• Anything beyond that is taxed at 40%

A simple example:

Let’s say your income is £60,270. This means:

• £12,570 is tax-free

• £37,700 is taxed at basic rate 20%

• £10,000 is taxed at 40%

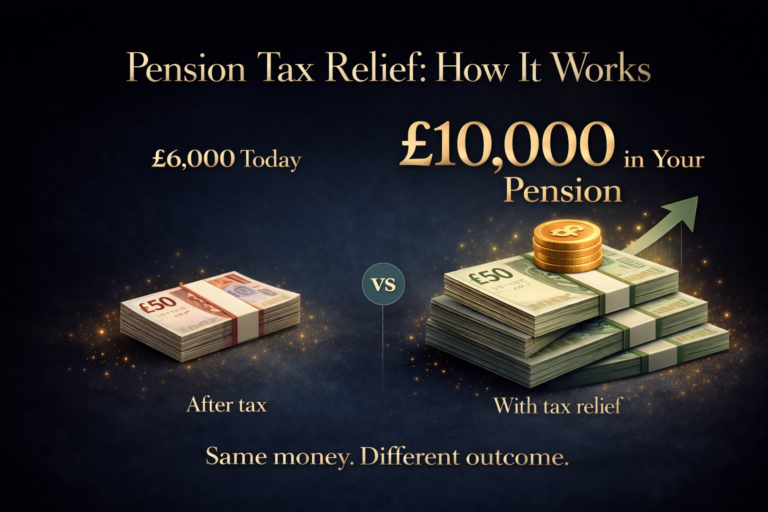

If you take that £10,000 as income, a large part of it goes to HMRC. In practice, you are left with around £6,000 (ignoring National Insurance for simplicity).

The alternative

Instead of taking that £10,000 as income, you could contribute it to your pension.

In that case:

• £10,000 it is not taxed at 40%

• tax relief applies

So instead of ending up with around £6,000 today, you could have £10,000 in your pension.

Same money, different outcome.

How pension contributions are handled

The way pension contributions are treated depends on how they are made. This will usually fall into one of the following categories:

Salary sacrifice (employees)

If your employer offers a salary sacrifice scheme, you agree to give up part of your salary, and that amount is paid directly into your pension. Because you never receive that money:

• No income tax is applied

• No employee National Insurance is applied

• Your employer also pays less employer National Insurance, and in some cases, this saving is added to your pension.

This is generally the most tax-efficient option available to employees. However, there are drawbacks to consider. Your contractual salary has been reduced, which may affect mortgage applications, borrowing capacity, and certain salary-linked benefits.

For example, if your salary is £68,000 and you sacrifice £10,000, your official salary becomes £58,000. This is often the figure lenders will consider.

Net pay arrangement (employees)

This works in a similar way to salary sacrifice, but with one key difference. You still pay National Insurance on your full salary. Income tax relief is applied automatically, but you do not benefit from National Insurance savings. Your contractual salary remains the same regardless of the pension contribution.

Relief at source (employees and personal pensions)

This is one of the most common arrangements, and often where people miss out.

Here:

• You receive your salary after tax

• You contribute to your pension from your net income

• The pension provider adds 20% tax relief

For example:

• £8,000 paid in becomes £10,000 in your pension.

• If your income exceeds £50,270, part of your income is taxed at 40%.

• This means you are entitled to additional tax relief.

• That additional relief is not applied automatically and must be claimed through self-assessment or by contacting HMRC

If it is not claimed, you are effectively overpaying tax.

I have seen many cases where the relief was simply not claimed.

Personal pensions (self-employed)

If you are self-employed, this is typically how contributions are made.

The same principles apply:

• you contribute from your income

• basic rate relief is added

• additional relief is claimed through your tax return

Pension contributions can also extend your basic rate band, meaning more of your income is taxed at 20% rather than 40%.

Company contributions (directors)

If you run a limited company, pension contributions can be made directly by the company.

This means:

• The contribution reduces company profits

• Corporation tax is reduced

• No PAYE or National Insurance applies

• The contribution is not treated as personal income.

This can be one of the most efficient ways to extract value from a company when structured correctly.

Who is most impacted

This tends to be most relevant for people whose income is approaching key thresholds.

For example, if your income is £60,270, the £10,000 above £50,270 is taxed at 40%. That is where the earlier £6,000 vs £10,000 example comes from.

You are more likely to be impacted if you fall into one of the following groups:

• Employees earning between £50,000 and £100,000 – This is where higher rate tax starts to apply, and pension contributions can make a noticeable difference.

• Parents receiving Child Benefit – Once income exceeds £50,000, the High-Income Child Benefit Charge starts to apply. This means some or all the benefit may need to be repaid.

Pension contributions can reduce your adjusted net income and may help reduce or eliminate this charge.

• Parents relying on childcare support – Certain childcare schemes are linked to income levels.

If income exceeds £100,000, access to some support can be lost. Pension contributions can sometimes bring income back below this level, restoring eligibility.

• Individuals approaching or exceeding £100,000 – This is where the personal allowance (£12,570) starts to be reduced. For every £2 earned above £100,000, £1 of personal allowance is lost. This creates what is often referred to as the 60% tax trap, where the effective tax rate becomes significantly higher than expected. Pension contributions can help reduce adjusted net income and preserve the personal allowance.

• Self-employed individuals and company directors – These groups often have more flexibility in how and when they make pension contributions, which can make planning particularly effective.

This is why timing and understanding your position before the end of the tax year can make a meaningful difference.

If you would like to discuss how this applies to your situation, you are welcome to book a tax consultation, and we can go through it together in a practical way.

Limitations

There are limits to be aware of:

• The annual pension allowance is currently £60,000 – this is the amount of pension contributions (employer’s + yours + tax relief) which receives tax relief. Unused allowances from the previous three tax years may be carried forward. Additional tax charges may apply if those limits are exceeded.

• Tax relief is limited to 100% of your UK earnings or £3,600 (whichever is higher)

Final thought

This is not about doing anything complex. It is about understanding how the system works and planning accordingly. If this applies to you, if you are unsure how this works in your situation, it is worth reviewing your position before the end of the tax year.